Myth-Busting Millennial Tropes: 8 Common Myths Busted

Millennials are faulted with killing off a myriad of things: department stores, paper napkins, ironing, and yes, even doorbells. A quick Google search reveals no shortage of things they have killed. Homeownership and the dream of homeownership, well, that’s not one of them. Let’s tackle some myths about Millennials, spending, and student debt.

Myth 1: Millennials do not want to buy a home.

Millennials are the largest adult generation today and they are the largest generation of home buyers at 37%. Millennials and first-time buyers face multiple challenges such as rampant competition in the housing market, low housing inventory, and buyers who are able to pay all cash for properties. While the homeownership rate for those under the age of 35 is lower than past generations at the same age, they are active in the housing market. They are also not all first-time home buyers. While 82% of millennials aged 22 to 30 are first-time buyers, the majority (52%) of older millennials aged 31-40 are repeat buyers.

Myth 2: Millennials just want to live in urban city centers and are priced out.

Urban centers are attractive with amenities, short commutes, and walkable locations. However, the majority of both older and younger millennials purchase in the suburbs. One-fifth of millennials purchase in small towns. This trend was true pre-covid, but the trend has been exacerbated with the ability to work remote. For all millennial buyers, the affordability of suburban areas is a driver. Younger millennial buyers place a top priority on being close to friends and family while purchasing.

Myth 3: Millennials rely on parent’s funds to buy homes.

This one has a kernel of truth to it. Twenty percent of older millennials aged 31 to 40 and 28% of younger millennials aged 22 to 30 did have a gift or loan from family or friends to buy a home. However, the majority use savings and nearly a third of older millennials use proceeds from their past home sale of a primary residence for the downpayment. Family also may help by allowing their young adult to double up prior to buying to avoid having to pay rent. This did occur for 28% of younger millennial buyers. It is possible this share has risen during the pandemic, but future data will tell the story.

Myth 4: Student loan debt is not holding back buying.

Among successful home buyers, 43% of younger millennials and 37% of older millennials had student loan debt, with median amounts of $25,000 and $33,000, respectively. These buyers were able to enter the housing market, but they did make financial sacrifices, found more affordable locations, and some did have parental help. Regardless of these decisions, having $25-33K of student loan debt erodes the ability to save for a downpayment and closing costs. Even among successful home buyers, the debt that did hold them back most from buying was student loan debt.

Buyers who had student debt purchase homes that were 19% less expensive than those without student debt, even when controlling for family help, size, and location of the home purchased. In a housing market with rapid and consistent price escalation, it is difficult to find a more affordable property to purchase.

When looking at student loan borrowers who do not own a home, 60% of millennials said student loan debt is delaying them from purchasing. Non-owners are being delayed from purchasing because they cannot save for a downpayment or closing costs, do not think they can qualify due to their debt-to-income ratio, don’t feel financially secure, and would not be able to make their mortgage payment in addition to their student debt payment.

Myth 5: Millennials are the only ones with student debt. Student debt is a millennial issue.

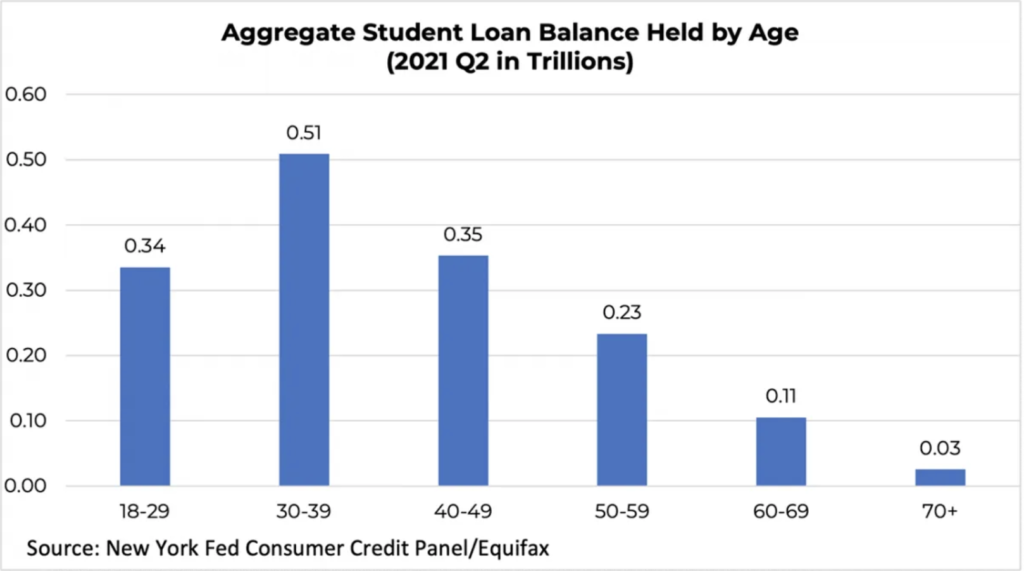

Student debt is an issue for ALL generations, not just millennials. More than 40 million Americans hold student debt. By age category, the closet proxy to generation, the highest aggregate amount of student debt is held by those who are 30 to 39 – thus in the older millennial generation. Those who are 30 to 39 hold $0.51 Trillion in student debt, the largest amount by age. Those who are 18 to 29 and 40 to 49 hold about one-third of a Trillion each in student debt.

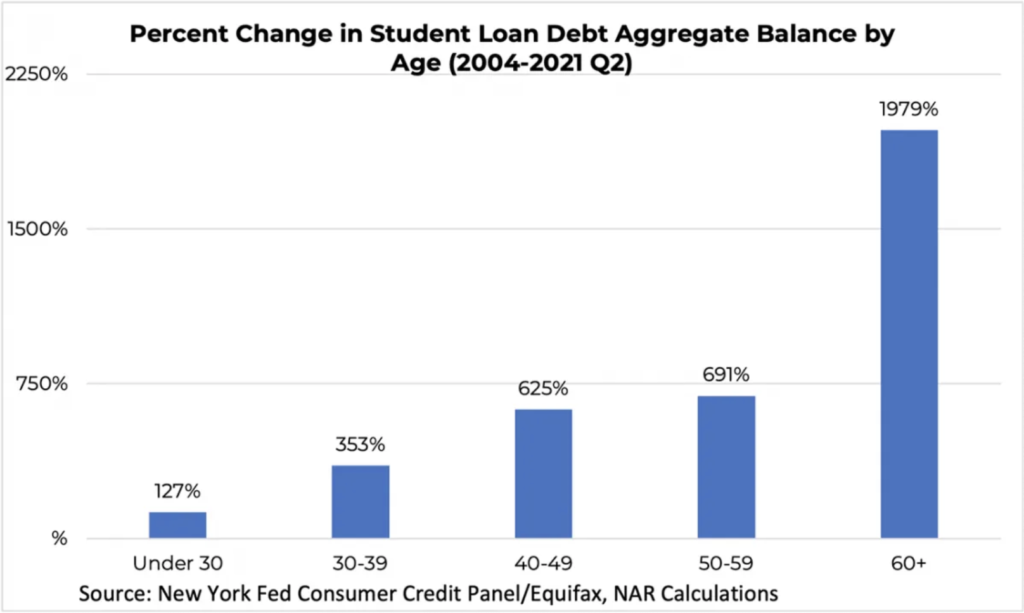

What is important to note when looking at student debt held by age is the growth in debt by those who are in older age categories. After the Great Recession, individuals went back to college, often reeducating themselves after job losses, and obtained a degree or certificate. People are living longer and often look to different career paths later in life. Individuals also take on student loans for children and dependents. Given these behavioral changes, the percent change in student debt held among those who are over the age of 60 has increased 1,979% since 2004, while the percent change among those who are under 30 with student debt has only increased 127%.

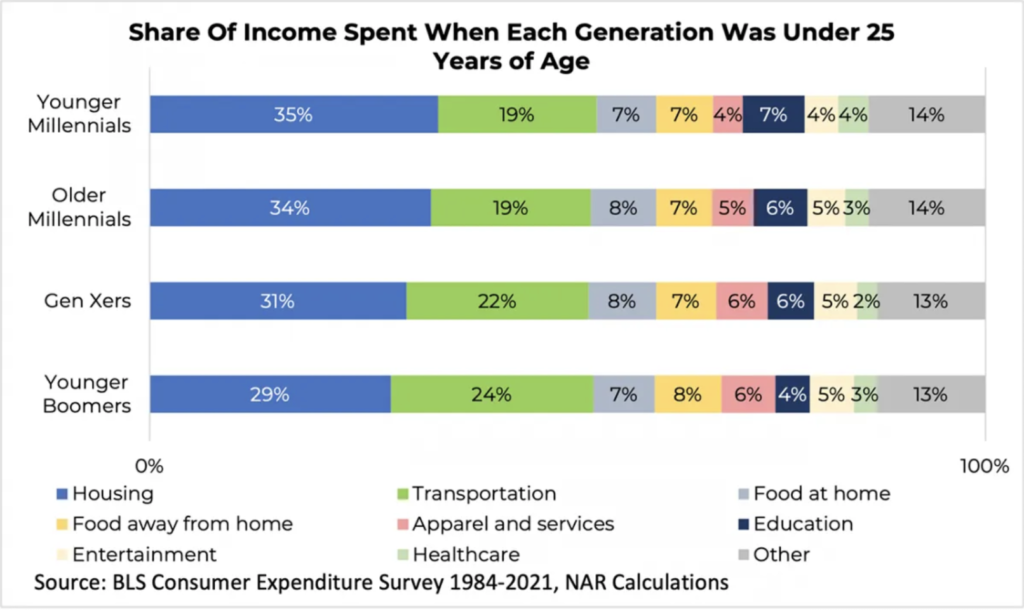

Myth 6: If millennials were just responsible with their money and stopped with their avocado toast, they could buy a home.

This trope, which started in Australia, has been paraded around for a number of years. When examining the data, however, it becomes clear avocado toast or any food eaten outside the home is not the issue. There is a shift in spending that is clear among younger generations to past generations at the same age. Younger Millennials are spending more on housing, education and slightly more on healthcare at the same age. Younger Boomers, in comparison, spent more on transportation, food away from home, apparel and services, and entertainment.

Myth 7: If student debt holders make more money, it will solve the issue.

One of the surprising findings from NAR’s new report on student debt was that even among those who did make over $100,000 a year, 60% cited their student debt was delaying them from purchasing a home. For these income earners, homeownership might seem within reach, but they still are delayed from moving forward due to the debt they are holding.

Myth 8: If student debt borrowers were able to pay down their debt, they would not actually buy a home and would continue living in their parent’s basement.

When asking questions about student debt and what a borrower would do, it’s important to note for many this may be a dream scenario and one they will have a difficult time accomplishing. Among the first priorities to those holding debt were long-term savings (43%), paying off other debt (40%), and investments (38%). Notably, 40% of student debt holders do not have an emergency savings fund of even $500. The fourth item was towards the purchase of a home (24%). This was listed above purchasing a car (22%) or even taking a vacation (21%)

Headship rates (the ability to move out of a parent/family member’s home) is impacted by student debt. After graduating from college 46% of all student debt holders were delayed, a share that rises to 75% among Gen Zers, and 62% among millennials. In comparison, only 37% of Gen Xers were delayed after obtaining student debt.